In a landmark decision on August 24, 2024, the Union Cabinet, led by Prime Minister Narendra Modi, approved the Unified Pension Scheme (UPS) for government employees. This new scheme represents a significant shift in how pensions are structured for public sector workers in India. Let’s dive deep into what this means for current and future government employees.

Background: Why the New Scheme?

Before we get into the details of the UPS, it’s important to understand why this change was needed:

- Balancing Act: The government has been trying to find a middle ground between the old pension scheme (which was generous but financially unsustainable) and the National Pension System (NPS) introduced in 2004.

- Employee Concerns: Many government employees have expressed concerns about the NPS, particularly regarding the lack of a guaranteed pension amount.

- Financial Sustainability: The government needs to ensure that pension commitments can be met in the long term without straining the national budget.

What is the Unified Pension Scheme (UPS)?

The UPS is a new pension plan that aims to provide financial security to government employees after retirement while maintaining fiscal responsibility. It combines elements of both defined benefit and defined contribution systems.

Key Features of the Unified Pension Scheme

Let’s break down each feature in detail:

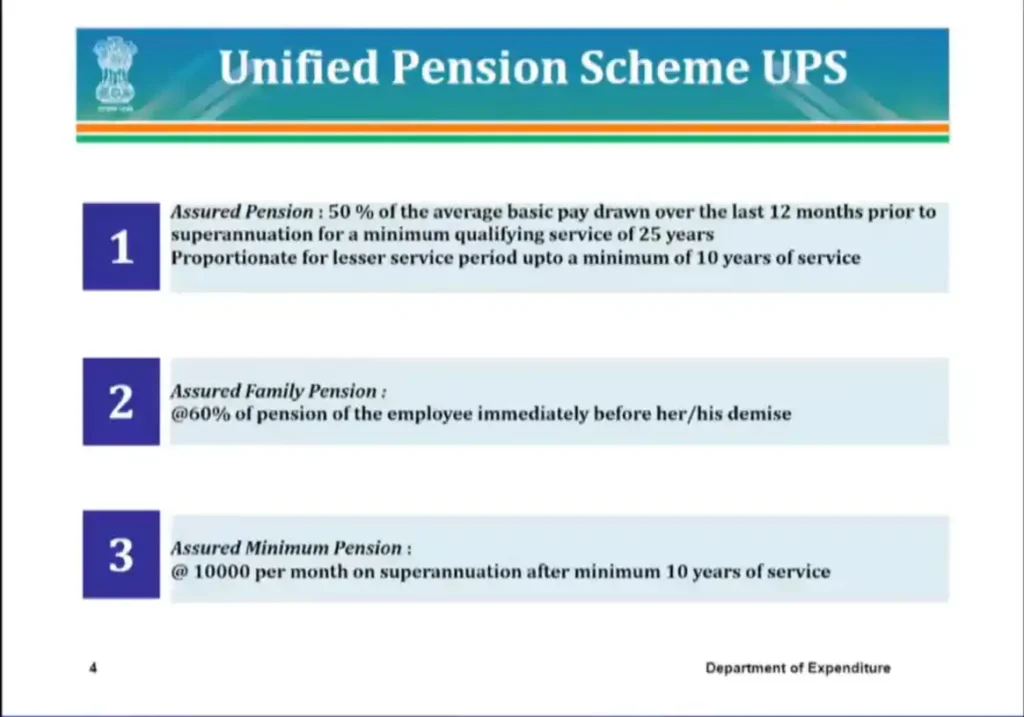

- Assured Pension:

- You’ll receive 50% of your average basic pay from the last 12 months before retirement.

- Minimum qualifying service: 25 years for full benefits.

- The pension is proportionately reduced for lesser service (minimum 10 years).

- Family Protection:

- 60% of your pension goes to your family if you pass away.

- This ensures your dependents are not left without financial support.

- Minimum Pension Guarantee:

- No less than ₹10,000 per month after 10 years of service.

- This sets a floor to ensure a basic standard of living for all retirees.

- Inflation Protection:

- Based on the All India Consumer Price Index for Industrial Workers (AICPI-IW), your pension will increase with inflation.

- This is similar to how Dearness Allowance (DA) works for serving employees.

- Extra Lump Sum Payment:

- At retirement, you get an additional one-time payment.

- Calculation: 1/10th of your last month’s salary (including DA) for every completed six months of service.

- This is on top of your regular pension and gratuity.

Implementation Timeline and Eligibility

- Start Date: April 1, 2025

- Who Can Join:

- All central government employees (approximately 23 lakh)

- Both recruits and existing employees have a choice

- State governments can opt to implement UPS for their employees (potentially benefiting up to 90 lakh people)

Choosing Between UPS and NPS

This is a crucial decision for employees. Here’s what you need to consider:

- UPS Benefits:

- Guaranteed pension amount

- Inflation protection

- Family pension assurance

- NPS Benefits:

- Potential for higher returns based on market performance

- More control over investment choices

- Option to withdraw a portion of the corpus at retirement

Remember, once you make your choice, it’s final. So, weigh your options carefully!

Impact on Government Finances

The government is increasing its contribution from 14% to 18.5% to support the UPS. This shows a significant commitment to employee welfare, but it also means increased financial responsibility for the government.

What About Past NPS Retirees?

In a noteworthy provision, the UPS will also apply to those already retired under the NPS. These retirees will receive arrears for the past period, with interest calculated at Public Provident Fund (PPF) rates. This retroactive application demonstrates the government’s commitment to equity among all its employees.

Frequently Asked Questions (FAQs)

- Q: Is joining the UPS mandatory?

A: No, it’s optional. You can choose between UPS and NPS. - Q: What happens to my NPS corpus if I switch to UPS?

A: The details haven’t been released yet, but your NPS corpus will likely be transferred to fund your UPS benefits. - Q: Will I have to pay more for UPS?

A: No, there’s no increase in employee contribution. The government is increasing its share. - Q: How does UPS compare to the old pension scheme?

A: UPS offers guaranteed benefits like the old scheme but with some elements of the NPS to ensure long-term sustainability. - Q: What if I leave my job before completing 10 years?

A: You might not be eligible for pension benefits, but you should be entitled to withdraw your contributions. The exact rules should be clarified by the government soon. - Q: Can I opt for UPS now and switch to NPS later?

A: No, once you make your choice, it’s final. Choose wisely! - Q: How will UPS affect government recruitment?

A: The assured pension might make government jobs more attractive, potentially increasing competition for these positions.

Conclusion

The Unified Pension Scheme represents a significant shift in India’s approach to public sector pensions. It aims to provide financial security to government employees while maintaining fiscal responsibility. As an employee, it’s crucial to understand the nuances of both UPS and NPS before making your choice.

Remember, pension decisions have long-term implications. Consider your risk appetite, family situation, and long-term financial goals. If you’re unsure, consider consulting with a financial advisor who can help you make an informed decision based on your individual circumstances.

The introduction of UPS shows the government’s commitment to employee welfare and responsiveness to NPS concerns. As more details emerge and the scheme is implemented, we can expect further clarifications and possibly some fine-tuning of the rules.

Stay informed, ask questions, and make the choice that best secures your financial future!